Institutional Insights: Credit Agricole FX Weekly 27/2/26

USD: Tech A Cold

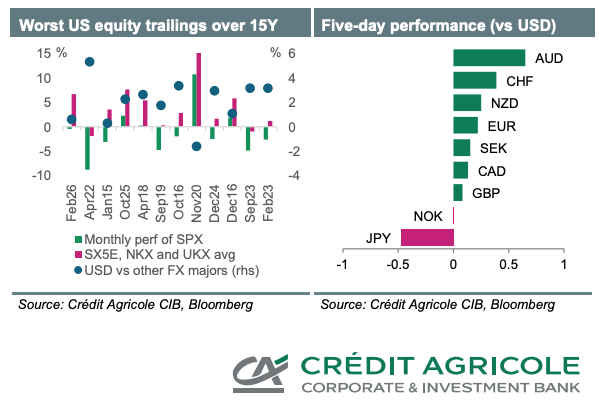

- Global markets showed little reaction to last Friday’s SCOTUS decision to overturn President Donald Trump’s IEEPA tariffs. In the G10 FX space, the USD has drifted without clear direction, largely overshadowed by other significant narratives. These include the disruptive potential of AI on certain business models and renewed concerns about the resilience of private credit markets. US equities, geographically concentrated, have struggled throughout the month, posting one of the largest monthly underperformances against other developed markets (DM) in years.

- The G10 FX market has responded to this divergence with the USD managing modest gains against other major currencies. At first glance, this outcome may seem counterintuitive, as one might expect equity and FX markets to align in reflecting cyclical shifts across major economies. However, our FAST FX model suggests that EUR/USD and USD/JPY exhibit a negative beta to relative equity performance. This supports the USD’s tentative rebound this month, implying that FX movements may have been influencing equity trends in recent months, particularly through the impact of significant FX shifts on the value of repatriated overseas earnings.

- Another factor supporting the USD’s relative strength could be FX hedging adjustments. In a scenario where US equities face losses while international equities see gains, international investors may unwind forward USD sales to cover reduced US equity exposure. Simultaneously, US investors might increase forward USD purchases to hedge against larger international equity exposure. Despite these dynamics, the USD’s gains this month appear modest given the scale of US equity underperformance—one of the most pronounced in the last 15 years. This leaves room for a more sustained USD recovery, especially if next week’s ISM surveys and February’s jobs report confirm the US economy’s resilience.

- Looking ahead, US-Iran talks are likely to remain in focus. Meanwhile, a slight expected uptick in February’s Eurozone CPI is unlikely to significantly impact the EUR, given steady ECB rates. However, Wednesday’s Swiss CPI data may hold greater importance for the CHF.

Disclaimer: The material provided is for information purposes only and should not be considered as investment advice. The views, information, or opinions expressed in the text belong solely to the author, and not to the author’s employer, organization, committee or other group or individual or company.

Past performance is not indicative of future results.

High Risk Warning: CFDs are complex instruments and come with a high risk of losing money rapidly due to leverage. 71% and 74% of retail investor accounts lose money when trading CFDs with Tickmill UK Ltd and Tickmill Europe Ltd respectively. You should consider whether you understand how CFDs work and whether you can afford to take the high risk of losing your money.

Futures and Options: Trading futures and options on margin carries a high degree of risk and may result in losses exceeding your initial investment. These products are not suitable for all investors. Ensure you fully understand the risks and take appropriate care to manage your risk.

Patrick has been involved in the financial markets for well over a decade as a self-educated professional trader and money manager. Flitting between the roles of market commentator, analyst and mentor, Patrick has improved the technical skills and psychological stance of literally hundreds of traders – coaching them to become savvy market operators!