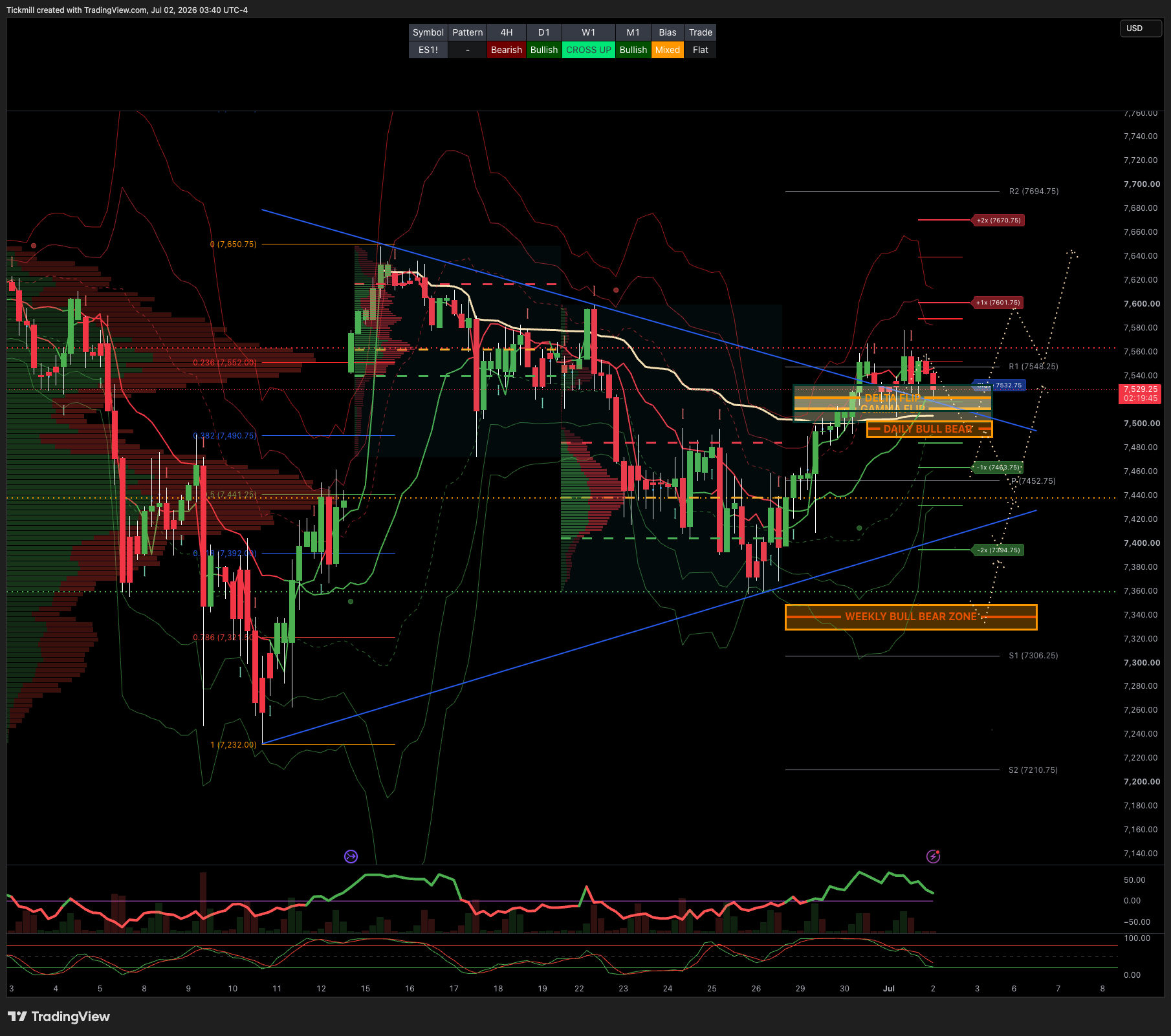

S&P500 Daily Action Areas & Price Targets 2/7/26

S&P500 Daily Action Areas & Price Targets 2/7/26

***QUOTING ES1! FOR CASH US500 EQUIVALENT LEVELS, SUBTRACT POINT DIFFERENCE***

WEEKLY BULL BEAR ZONE 7350/40

WEEKLY RANGE RES 7280 SUP 7520

MONTHLY RANGE RES 7932 SUP 7384

JHEQX Q3 Collar Short Call Cap: ~7,750 – 7,900 - Long Put Strike: ~7,050 – 7,100 (approx. 5% downside protection) Short Put Strike: ~5,950

DEC2025 OPEX to DEC2026 OPEX is 945 points giving us a range of [5889,7779]

SPX PUT/CALL RATIO 1.02 (The numbers reflect options traded during the current session. A put-call ratio below 0.7 is generally considered bullish, and a put-call ratio above 1.0 is generally considered bearish.

DAILY VWAP BULLISH 7440

WEEKLY VWAP BULLISH 7494

MONTHLY VWAP BULLISH 7036

DAILY STRUCTURE - OTFH 7495

WEEKLY STRUCTURE - BALANCE 7648/7247

MONTHLY STRUCTURE - OTFH - 7199

Balance: This refers to a market condition where prices move within a defined range, reflecting uncertainty as participants await further market-generated information. Our approach to balance includes favouring fade trades at the range extremes (highs/lows) while preparing for potential breakout scenarios if the balance shifts.

One-Time Framing Higher (OTFH): This represents a market trend where each successive bar forms a higher low, signalling a strong and consistent upward movement.

One-Time Framing Lower (OTFL): This describes a market trend where each successive bar forms a lower high, indicating a pronounced and steady downward movement.

DAILY BULL BEAR ZONE 7490/7500

GAMMA FLIP 7512

DELTA FLIP 7522

DAILY RANGE RES 7611 SUP 7424

2 SIGMA RES 7680 SUP 7404

VIX BULL BEAR ZONE 17.4

TRADES & TARGETS

LONG ON REJECT/RECLAIM DAILY/MONTHLY BULL BEAR ZONE ***ACTIVE POSITION***

LONG ON REJECT/RECLAIM DAILY BULL BEAR ZONE TARGET DAILY RANGE RES

***ADDITIONAL SETUPS & TARGETS HIGHLIGHTED ON THE CHARTS***

(I FADE TESTS OF 2 SIGMA LEVELS ESPECIALLY INTO THE FINAL HOUR OF THE NY CASH SESSION AS 90% OF THE TIME WHEN TESTED THE MARKET WILL CLOSE ABOVE OR BELOW THESE LEVELS)

GOLDMAN SACHS FICC & EQUITIES TRADING DESK VIEWS

Market Recap — Momentum Unwind, Not Index Breakdown

US equities finished modestly lower, but the headline index move understated a much larger factor rotation beneath the surface. The S&P 500 fell 22bps to 7,488, while the NDX declined 154bps to 29,809, the Russell 2000 lost 26bps to 3,016, and the Dow was essentially flat at 52,305. Volumes were close to normal at 19.403bn shares versus a YTD daily average of 19.724bn, and the close again saw a $1.3bn MOC to buy. The index drawdown was contained, but the underlying factor move was not: high-beta momentum fell nearly 10% after ending the first half up a record 57%.

The day’s core story was a momentum unwind triggered by renewed consolidation across AI names, including a 2% decline in the KOSPI overnight. This was not a broad risk-off session. It was a sharp rotation out of the most extended AI bottleneck and supplier winners and back toward a more balanced set of exposures, including hyperscalers, software, cyclicals, and other laggards. That distinction matters. The index held in relatively well because breadth is improving, but crowded momentum books suffered because leadership is beginning to broaden.

This fits the H2 setup almost perfectly: long delta / long vol remains the right conceptual posture, but the path is becoming more hostile for crowded factor expressions. The high-beta momentum basket entered the summer with enormous gains, elevated realized volatility, and a highly crowded ownership base. Tougher summer seasonality, crowded positioning, high factor volatility, and the broadening trade all argue that momentum can struggle in the short term even if the S&P itself remains resilient. In other words, the market can go sideways to higher while the most crowded long/short books experience real pain.

The breadth improvement is important. A catch-up rally in lagging cyclicals, software, consumer stocks, or housing could support the index while simultaneously pressuring crowded AI/momentum portfolios. That is exactly the type of environment where headline beta does not tell the full story. If laggards rally and prior winners consolidate, index-level drawdowns can stay shallow, but factor-level drawdowns can be severe. This is especially true after a first half defined by right-tail winners in memory, data centers, AI semis, Korea, Taiwan, and Japan.

Cross-asset signals were mixed but not alarming. VIX rose only 97bps to 16.59, despite the violent momentum move. WTI fell 212bps to $68.09, easing energy pressure. The 10-year yield rose marginally to 4.4791%, gold gained 64bps to 4,033, DXY firmed 21bps to 101.40, and Bitcoin rose 220bps to 59,926. This was not a classic macro liquidation. Oil was lower, rates were stable, the dollar was slightly stronger, and vol barely moved. The evidence points to an equity-internal rotation rather than a macro shock.

Warsh’s appearance at Sintra was a non-event, which is notable in itself. Markets had some concern that his first major international appearance as Fed Chair could introduce fresh volatility or a more hawkish tone, but the event passed without meaningful disruption. Cooler Eurozone CPI was also supportive at the margin, while US ISM remained strong despite printing below consensus. The macro picture remains consistent with moderate growth, contained but sticky inflation, and a Fed that is less committed to forward guidance but not yet forced into a new tightening cycle.

The next key macro catalyst is NFP. The expectation is for a +130k headline payroll gain in June, above consensus of +115k but close to whispers around 137k. The unemployment rate is expected to remain unchanged at 4.3%, reflecting stabilization in continuing claims, while average hourly earnings are expected at +0.2% MoM, below consensus of +0.3%, partly due to negative calendar effects. A print near those numbers would likely be acceptable for risk assets: enough job growth to support the soft-landing narrative, but not enough wage pressure to reprice the Fed materially more hawkish.

The more interesting macro point may come next month. With less noise from Iran and commodity price volatility, ISM and inflation data could provide a cleaner read on whether growth is inflecting higher. If US activity data remain firm while oil stays contained, the market can continue to support cyclicals and broadening. That would reinforce the shift away from narrow AI leadership and toward a more pro-cyclical tape.

Flow activity remained muted ahead of the US holiday. The floor was only 3 out of 10 on activity, but still finished 356bps to buy versus a 30-day average of 47bps to buy. Asset managers were roughly flat, with supply in Communication Services and Industrials offset by demand in distortionary flows. Hedge funds were net buyers, with scattered demand across sectors excluding Tech and Energy. This is consistent with a rotation rather than de-risking: investors are not abandoning equities, but they are changing what they want to own.

The derivatives tape also confirmed the factor-rotation story. NDX spot and vol traded positively correlated, with vols offered across the surface despite NDX underperformance. That means investors were not aggressively bidding protection into the tech decline. Instead, implied volatility softened as the move was treated as a positioning unwind rather than a new downside regime. Skew relaxed in both NDX and RUT, while SPX skew was modestly bid. Flows were slower overall but tilted toward buyers of forward vol, which fits the “stay invested but own convexity” framework.

The large S&P 31Aug 7000/7950 strangle in roughly $20mm vega / $115mm premium is worth flagging. That trade expresses the market’s recognition that the second half has wider outcome distributions: downside risk if AI, earnings, or rates disappoint, but upside risk if July seasonality, earnings growth, and broadening continue. This is very consistent with a long-vol mindset around a still-positive directional market.

On the micro/thematic side, options flows were dominated by software, IGV, and broader Mag7. The tilt toward upside buyers suggests investors are beginning to look for recovery trades in lagging areas of Tech, particularly after the heavy de-rating of hyperscalers and software versus the AI supplier complex. This is a meaningful development. If investors are rotating from AI bottlenecks back into hyperscalers/software, the “AI recipient versus AI spender” trade may be entering a consolidation phase, at least tactically.

The key tactical message is that momentum is vulnerable, but the index is not necessarily broken. The S&P remains close to recent highs, VIX is contained, oil is lower, and breadth is improving. But the leadership structure is shifting. The huge first-half gains in memory, AI semis, data centers, Korea, Taiwan, and high-beta momentum create room for sharp reversals without requiring a bearish macro view. A market that broadens into cyclicals, software, consumer, housing, and selective hyperscalers can still produce decent index returns while creating a difficult backdrop for crowded long winners / short laggards books.

For positioning, that argues for reducing dependence on the most crowded momentum expressions and leaning into a more balanced barbell: retain quality AI infrastructure exposure, but pair it with recovering hyperscalers, software, industrial cyclicals, and other laggards with improving earnings revisions. Avoid treating every AI supplier pullback as an automatic dip-buy, particularly where ownership remains elevated and first-half returns were extreme. At the same time, avoid becoming outright bearish on the index when the rotation itself may be healthy.

The immediate risk is tomorrow’s payrolls report. A Goldilocks print would likely support the broadening trade and keep VIX contained. A hot payrolls/wage number could pressure duration-sensitive growth and revive Fed hike fears. A weak labor print could test the soft-landing narrative, though lower yields might cushion parts of growth. Given the shortened week, thin liquidity, and a 0.60% implied move through week-end, even a modest surprise could produce an outsized reaction

Disclaimer: The material provided is for information purposes only and should not be considered as investment advice. The views, information, or opinions expressed in the text belong solely to the author, and not to the author’s employer, organization, committee or other group or individual or company.

Past performance is not indicative of future results.

High Risk Warning: CFDs are complex instruments and come with a high risk of losing money rapidly due to leverage. 69% and 73% of retail investor accounts lose money when trading CFDs with Tickmill UK Ltd and Tickmill Europe Ltd respectively. You should consider whether you understand how CFDs work and whether you can afford to take the high risk of losing your money.

Futures and Options: Trading futures and options on margin carries a high degree of risk and may result in losses exceeding your initial investment. These products are not suitable for all investors. Ensure you fully understand the risks and take appropriate care to manage your risk.

Patrick has been involved in the financial markets for well over a decade as a self-educated professional trader and money manager. Flitting between the roles of market commentator, analyst and mentor, Patrick has improved the technical skills and psychological stance of literally hundreds of traders – coaching them to become savvy market operators!